Contents

Investing for the future can be an intimidating experience. What should you invest in? Who should you invest with? There are so many options that one can easily get stuck like a deer in the headlights.

Of the many different options on offer, Hargreaves Lansdown is probably one of the best-known investment firms in the UK. They’re also one of the few institutions to offer a Stocks and Shares (S&S) Lifetime ISA. So it was that I recently put my faith in them and opened a LISA to save for the future.

This review is for anyone considering taking out a Lifetime ISA. It is especially for those weighing up the alternatives and thinking about opening a Stocks and Shares LISA with Hargreaves Lansdown.

What follows are my personal opinions. I have not been paid to write this Hargreaves Lansdown Lifetime ISA review. Indeed, the company have no idea I am writing this (though maybe their marketing department will stumble across it at some point!). In other words you’ll get to hear the unadulterated reality – both the good and the bad.

Before we start I should reiterate that these are just my experiences. Yours may differ. As may your returns. Nothing here should therefore be considered financial advice. More of a journal entry. So with that said let’s dive into the world of Lifetime ISAs…

Why I Chose Hargreaves Lansdown

My purpose in opening a Lifetime ISA is to save money for my retirement. I’m willing to lock my money away for decades in the future, trusting that compound interest, government bonuses and stock market growth will give me a comfortable lump sum in later life. It’s certainly not the only plan I have to fund my retirement, but it’ll be a nice little bonus at the age of 60.

I chose a Stocks & Shares LISA because I’m willing to shoulder the higher level of risk in exchange for the potential of higher returns. I am banking on the extended time over which the money will be invested to ride out any market drops.

So why Hargreaves Lansdown? Well, firstly they’re one of the few companies to offer a S&S Lifetime ISA. Secondly, they are one of the largest investment firms in the UK which gives me faith that they know what they’re doing. I wouldn’t half as comfortable investing with a tiny company I’d never heard of.

Thirdly they offer good amounts of flexibility in how you can invest your money. There are lots of funds to choose from so you can create a portfolio that matches your risk profile.

Opening a LISA with Hargreaves Lansdown

The first thing that I found surprising about Hargreaves Lansdown is that they don’t seem to be the most technically-savvy company. In this online age, their automated systems weren’t able to identify me as genuine, so I had to print out paper forms, fill them in and post them off.

I use snail mail so rarely that it’s very unusual if I can remember where my stamps are. At the very least I would expect to be able to upload my application form to their website or email it to them. But no.

I’m sure I was unlucky. I had only recently moved house, so I accept that I wouldn’t have been on the electoral role at that point. You’ll probably be perfectly successful at opening an account online.

While the experience of posting off forms felt unusually old fashioned, it was only really a tiny glitch, and certainly not enough to stop me opening an account with them.

ISA Transfers

While opening my LISA with Hargreaves Lansdown I also wanted to transfer in an old Help to Buy ISA to kick-start my savings. Again – something that should be oh-so-simple. But – again – another old fashioned paper form to print out and fill in.

I completed it and – with my last first-class stamp – posted off the forms.

Then I waited.

And waited some more.

And finally after some weeks I got bored waiting and rang up to discuss the situation. I was told there was no record of my transfer request in my account. Apparently they hadn’t received the form.

I asked if I could initiate the transfer over the phone.

No, they needed the form.

So, after buying another book of stamps, I printed out the forms again and filled them in again. And posted them off again.

And waited.

And waited.

And then reached out once again. Still no forms had been received.

Can you guess what I did next?

Yep, I printed out and posted off some more forms.

A week or two later I finally received written confirmation from the Hargreaves Lansdown transfer team that they had received my request.

The transfer actually happened very quickly and smoothly after this point. I was very happy with the process, though it felt oddly old fashioned to receive printed letters in the post from Hargreaves Lansdown about the transfer.

And while I mock the repeated form filling I of course cannot say for certain that Hargreaves Lansdown lost my forms. Perhaps they got lost (or stolen?) in the post?

Frustrating but not the end of the world.

Lifetime ISA Government Bonuses

In case you’re wondering how the government incentives work with a Lifetime ISA, Hargreaves Lansdown deal with all this on your behalf. No need to lift a finger.

Some weeks after paying money into your LISA you’ll see the 25% bonus land in your account.

![]()

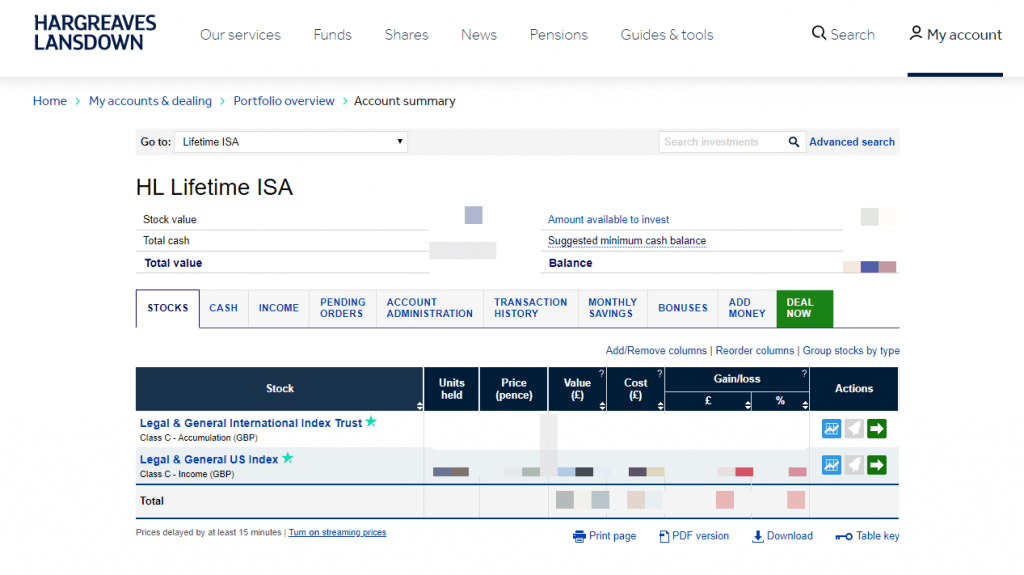

You can check your transaction report at any time within the Hargreaves Lansdown platform to confirm the bonuses are being credited correctly.

Hargreaves Lansdown Investment Platform

While I was surprised by the amount of paperwork in the early stages of opening my LISA, after this point most of your activity will occur via the Hargreaves Lansdown website. You can check the balance of your account, pay in money, make investments and more. It’s quite a nice platform in my opinion – fully-featured without being intimidating.

In order to set up your account you’ll need a unique pin, which will be sent to you. Unfortunately mine didn’t arrive (more postal problems?) so I had to ring up and get the details. Fortunately this was a reasonably painless process and I was soon logged into my account.

I may have an unhealthy interest in personal finance but I most certainly am not an expert when it comes to investing.

I mention this because I assumed that investing in a S&S LISA was just like adding money to a savings account. You pay money in and then the financial institution uses it’s wizardry to grow that money over time.

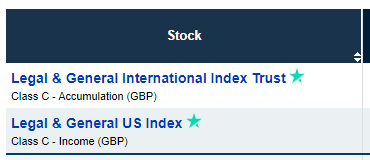

I was therefore rather surprised that with the Hargreaves Lansdown Stocks and Shares LISA you get to choose where your money goes.

What would you like to invest in?

This offers a good degree of flexibility and control.

It also means, however, that you’re going to have to do some research and try to choose which funds to buy into. For beginners (like me) this can be rather intimidating. So if you opt for a Hargreaves Lansdown S&S LISA be prepared to sit down for a few hours at some point to investigate your various options.

Personally I opted for some index funds, with the intention of spreading my money across a diverse range of companies. Hopefully this will minimise my risk.

Luckily the Hargreaves Lansdown site provides lots of information on the different funds they offer so you’re not investing blindly. Making your “trade” is very simple – you decide how much to invest and in which fund. Click a few buttons and you’re all done.

A few days later you receive confirmation of the successful investment – by post of course.

I don’t know why but I felt incredibly grown-up when my first purchase confirmation came through!

Communication from Hargreaves Lansdown

We’ve mentioned Hargreaves Lansdown’s love of snail mail already, but how do their other communication channels measure up?

Firstly, in the difficult process of opening my account and transferring my ISA over I spoke to Hargreaves Lansdown on the phone several times. I can tell you that the service was exceptional in every way. The phones were answered incredibly quickly, the people I spoke with were consummate professionals and couldn’t have been more helpful or polite. At this point my experience of dealing with Hargreaves Lansdown over the phone could not be improved upon.

Email is a little more hit-and-miss in my experience. For example, just yesterday I received an email encouraging me to activate my online account – despite the fact that I have already been using it for months already.

My personal opinion is that Hargreaves Lansdown is trying very hard with their communication. The call centre seems excellent. I like to receive my trade notices. There are, however, some teething problems that I experienced along the way. Certainly not enough to put me off Hargreaves Lansdown, but hardly the sort of thing I’d expect from a company of this size.

In fairness, the issues have primarily involved snail mail. Who knows how many people’s hands these letters pass through before completing their journey from sender to recipient? Each one of those people could misplace a letter. So let’s give Hargreaves Lansdown the benefit of the doubt on this one.

Hargreaves Lansdown LISA Review Conclusion

Now that we’ve discussed my experiences of Hargreaves Lansdown at some length I suppose the most important question is whether I’m happy with the experience. To this end I would say “certainly”. It certainly hasn’t been without its hiccups, but these may in reality not be anything to do with Hargreaves Lansdown.

I’m happy with my experiences so far, and I still have faith in Hargreaves Lansdown as a big, reliable investment firm that I’m happy to leave my money with. In the next few years I’ll be looking to open a new standard ISA, and as things stand I’m likely to open it with Hargreaves Lansdown. I suppose that’s really the proof of the pudding.

Do you use Hargreaves Lansdown? What have your experiences of opening a LISA been to date? Please leave your thoughts, opinions and experiences in the comments section below so other readers can benefit.

Add comment